Why EDF's Hinkley C nuclear power plant will probably not be running before 2035

There is a broad relationship between the time it takes to build nuclear power stations and their cost. That is apparent from looking at what has happened in the past, with nuclear costs escalating as construction times have increased. A study of this relationship leads to the conclusion that the commercial operation of Hinkley Point C (HPC) will almost certainly not happen before 2035.

The model being built at Hinkley C is the European Pressurised Reactor (EPR). The only two EPRs to have been (more or less) completed in the West have involved major cost overruns. They have taken much longer to build than expected. In Finland, the plant at Olkiluoto took nearly 17 years to come into commercial operation from its construction start in 2005. The EPR at Flamanville in France has so far taken 17 years to (not quite as yet) come into commercial operation since the concrete for the reactor was first poured in 2007.

When I was writing a book about nuclear power, safety, and costs I did an (anonymised) interview with a British-based nuclear industry consultant who commented:

‘the point at which you do the first concrete pour, the organisation starts hemorrhaging money. That is when you have to build as rapidly as possible with minimum delays and commission as quickly as you can'. (anonymous interview with nuclear consultant, 01/06/2018) (page 133 see book link HERE ). It’s a simple relationship really. The longer the construction period is, then the longer you have to employ staff to do the job. Hence costs increase almost as night follows day.

You can see the relationship between costs and construction time in Figure 1 below. Please note these are so-called ‘overnight’ costs and do not include interest payments to debtors or equity holders. This, in reality, pushes up costs greatly, which is why these ‘overnight’ costs greatly understate nuclear costs. However, I use the overnight costs for comparison purposes, and also because their interpretation is much more transparent and unarguable compared to making assumptions about the cost of capital.

Figure 1 Comparison between cost per GW €bn (2024) and years under construction of Flamanville and Olkiluoto EPRs -

Yellow shows ‘overnight’ costs in euros per GW, blue shows the construction time in years

Sources of Data: International Atomic Energy Agency Power Reactor Information service (PRIS), and World Nuclear Industry Status Reports 2019 and 2024

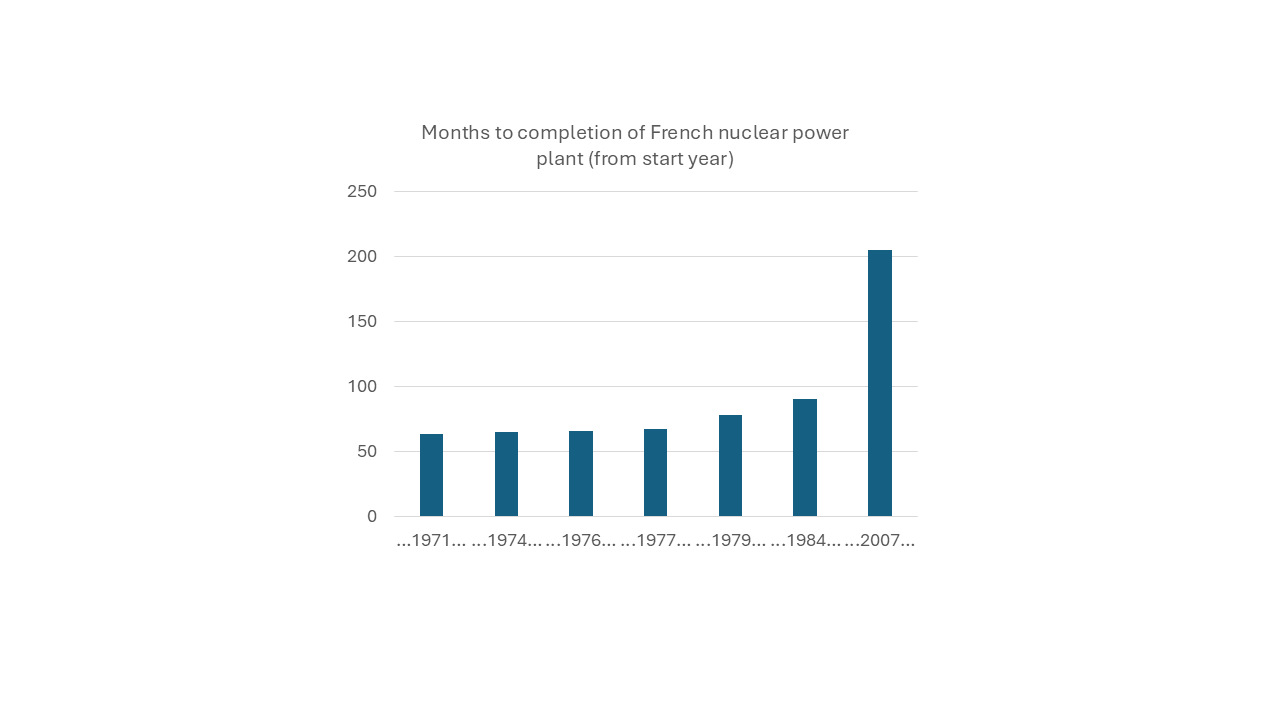

In a post earlier this year I explained how Flamanville 3’s construction time had been part of a trend towards increasing nuclear construction times in France. This is shown in Figure 2 below. The bar on the right represents Flamanville 3 whose construction began in 2007.

Figure 2 Months to completion of reactors in France from different start dates

Data up until Flamanville taken from : Source: Grubler, A (2010) The costs of the French nuclear scale-up: A case of negative learning by doing, Energy Policy Vol 38 5174–5188, Table 1 p 5755

Both the power plant compared in Figure 1 (Flamanville 3 and Olkiluoto 3) cost much more than expected. However the alarming thing about the British nuclear programme is that they are still only about half as expensive as the projected costs of Hinkley C. Whereas Olkiluoto 3 and Flamanville 3 have overnight costs of around 8.7 to 8.1 billion euros per GW, Hinkley C has projected costs, according to EDF, of around double this amount (ie over 16 billion euros per GW) when EDF’s median projected costs are translated into 2024 euro prices. (See HERE for costs in 2015 £s, as reported by ‘World Nuclear News’).

This does imply that Hinkley C is going to take even longer to come online than these power plants in Finland and France did. Hinkley C’s reactor construction began at the end of 2018, and the cost estimates made then were broadly in line with the sort of costs we have seen in the cases of Fimamanville and Olkiluoto. However, projections of cost overruns for HPC have escalated since then.

Even if EDF ‘only’ took as long to build as Flamanaville and Olkiluoto, HPC will not be online until 2035. But the costs of HPC are much higher, around double, compared to either of these other EPRs. Of course, we cannot say, for definite, now how long for sure completion of HPC will take. But we can do an estimate by working backward from the cost. That is if there is a simple linear relationship between construction time and cost then we could say that if HPC is going to cost twice as much as Flamanville 3 or Olkiluoto 3 then HPC will take twice as long as these plants - that is well over 30 years. On that basis, HPC would not be finished until around 2050. You can see this calculation in Figure 3. HPC is in the third set of columns

Figure 3 Estimated construction time needed to finish HPC working backward from relationships between costs and construction times of Flamanville 3 and Olkiluoto 3

Data sources : see sources for earlier charts

Maybe it will not take quite as long as 2050 to finish HPC - I cannot say - but what these simple calculations do suggest that EDF’s (most recently) projected completion dates of 2029-2031 look hopelessly optimistic. Even if HPC ‘only’ takes as long as Flamanville 3, we shall still be looking at a start no earlier than 2035. The CEO of EDF is famously quoted as saying that people would be cooking their turkeys by the xmas of 2017. We could be lucky to be cooking our turkeys using HPC power by 2037!

The prospect of HPC not being online in 2029 automatically triggers penalty clauses in the contract that was agreed between the UK Government and EDF in 2013. If EDF does not meet this deadline then it loses a year of its premium price guarantee for every year that it fails to start generating. The premium price of £92.50 per MWh in 2012 prices which equates to £129 per MWh in 2024 prices. No doubt pressure will grow on the UK Government to relax the penalty clause.

All of this does not bode well for Sizewell C. This is a carbon copy of the design of HPC, we are told. Except that it is not, It is on a different site with its own, different, challenges. There can be no confidence that the costs will be much less than HPC - as Amory Lovins puts it, nuclear power seems to have an ‘unlearning curve’ - ie it gets more expensive over time in a given country. It is unlikely that EDF will have much capacity to do much on Sizewell C until HPC is more or less completed, and as Sizewell C is likely to take at least 15 years to build (based on experience with EPRs) it seems unlikely that Sizewell C will be generating this side of 2050. I have one good reason to hope to see the day when Sizewell C is generating. It means that I shall live a very long time and be very old indeed!

Otherwise, it would not be wise to persevere with Sizewell C. Sizewell C is likely to come online when it is even more technologically uncompetitive than it is now with other green energy sources and techniques. Indeed the approach of the Government has altered dramatically since the Hinkley Point C contract was signed. Then there were penalty clauses imposed on EDF to encourage good performance. Now, with Sizewell C, EDF will be able to rely on the consumer to pay the tens of billions of pounds of cost overruns that will inevitably occur. A sort of reverse logic has been applied. It has been realized that nuclear power is too uneconomic to be built by offering a long-term contract to buy electricity. But instead of walking away from the technology, we will now take on a massive uncapped financial obligation for the next project.

In June 2025 The UK Government announced funding dispensations for Sizewell C and also so-called ‘small modular reactors’. I produced the following graphic the give the comparison between planned spending on new renewables and new nuclear power. No further comment is necessary!

Staggering numbers. I remember the 2017 Christmas turkeys promise. Whatever happened to Vincent de Rivaz..?!

There are two reactors at Hinkley so maybe 2035 is reasonable for the 2nd unit although how an earth we get from Calder Hall built in under 4yrs 70yrs ago to the Hinkley timescales given all the modern construction plant and techniques now at our disposal is beyond me.

We should have bought the Sth Korean design which is have to be quicker to build and less costly although again another example of how the UK has sunk so low in its engineering capability from being world leaders to world laggards.