Why have UK energy prices been so high? Privatisation and liberalisation is largely to blame

What is the standard answer as to why the UK suffered so much of a gas and electricity price shock in 2022 and thereafter? People will say it is because of the effects of the Ukraine War and Europe’s reliance on global gas prices. I am not going to argue against this as an immediate cause. However it is clear to me that things would have been a lot better for the UK if gas and electricity privatisation and liberalisation had not taken place. Without this the UK would have has much lower gas and electricity prices since 2021.

The laws that put privatisation and liberalisation in place occurred during the Thatcher period. These new laws removed the control that the nationalised industries had over how much they paid for gas sourced from the North Sea. Previously the oil and gas companies that drilled the North Sea did so under UK license requirements that they could only sell the gas to the nationalised British Gas Corporation. British Gas had a ‘monopsony' which meant that the oil and gas companies could only sell to them, and therefore take the prices they could negotiate with British Gas. This meant that if there was an energy price spike, the oil and gas companies could not then seek the higher world prices. They had to sell on the basis on what they could agree with British Gas. They would not be able to pocket the ginormous returns that they have received since 2021.

This is a difficult-to-contest fact that you do not hear mentioned very much. After all we live among a dominant discourse that privatised, and liberalised market arrangements will automatically generate the best outcomes for the consumer. However where there is a strictly limited resource, as in the case of North Sea Gas, or indeed fossil fuel resources in general, this is not necessarily the case.

Nowadays of course it does not make much, if any, difference to the gas prices the consumer pays whether North Sea gas is run down sooner or later - or whether fresh fields are exploited or not. That is because British consumers pay world liquified natural gas (LNG) prices. The European gas market has not been self-sufficient for a long time, and so is reliant on these world LNG prices to set the price for all wholesale gas. But if the industry had not been privatised and liberalised then the price of gas from the UK North Sea would have been decided democratically by the UK Government.

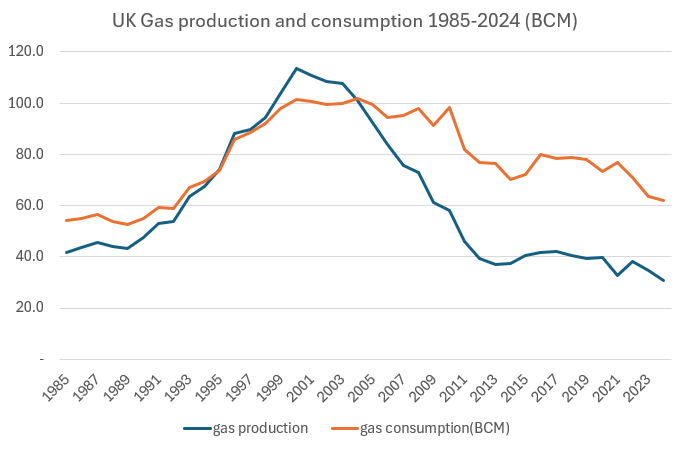

Figure 1 shows natural gas production from UK’s part of the North Sea compared to UK consumption of natural gas. As you can see both production and consumption of natural gas took off after the 1987 privatisation of British Gas and then (in 1991) liberalisation of North Sea gas contracting. Liberalisation meant that the rules preventing oil and gas companies selling on the wider European or world market were scrapped. This was good news for the oil and gas companies who could now sell a lot more gas. Eventually it ended up being very bad for the consumer and the environment in general. This is because not only consumers end up being soaked by the oil and gas companies in the recent crisis, but also the use of natural gas (and the consequential carbon emissions) was encouraged.

Figure 1

Source: Energy Institute Statistical Review of World Energy

Crucially, the abolition of the British gas monopoly of use of gas allowed independent companies to access gas and use it to supply new gas fired powered stations. In parallel to this the existing nationalised Central Electricity Generating Board was split up and privatised. Combined cycle gas turbines (CCGTs) were at that time a new technology. They combined a gas turbine with a steam turbine. The steam turbine utilised otherwise waste heat to increase the rate of conversion of gas into electricity. Matched with the privatisation and (at first partial) liberalisation of electricity markets, this meant that CCGTs could now be deployed. This possibility was seized by independent companies working with newly privatised regional electricity companies. This dramatically increased the levels of gas consumption in the UK.

You can see how gas generation increase after 1990 in Figure 2. This rose to around half of UK generation by the year 2000, a position which it, very broadly speaking, maintained until recently. Wind and solar production have increased, first effectively substituting for coal. Now they are starting to substitute for gas,

You will note that I have left out (from Figure 2) generation from nuclear power, biomass and hydro from this graph. This is to enable us to focus attention on the biggest changes in generation proportions, and to illustrate the rise of generation from gas. The combined proportion from nuclear, biomass and hydro have been very broadly stable over large parts of the period. Nuclear power generation rose, and then fell this century. However this fall has been offset by increased biomass production, with hydro generating little more than 1% of production throughout.

Figure 2

Source: Energy Institute Statistical Review of World Energy

Figure 3

In Figure 3 I have subtracted the fuel used by the CCGTs from UK gas consumption. I have done this to illustrate what UK gas consumption would have been without the CCGTs. You can see that if this was the case, and there had been no or little use of CCGTs, then in 2022 more than 80 per cent of UK gas consumption would have been covered by gas from the North Sea.

Because of the British Gas monopsony (if it has been maintained) the oil and gas companies in the UK North Sea would have had no option but to sell to British at a pre-arranged, contracted, fixed price. The oil and gas companies would not have been able to bargain a higher price simply because the global liquified natural gas (LNG) prices had spiked.

Source: Adapted from data in Energy Institute Statistical Review of World Energy - assumed CCGT conversion efficiency 48%

Let us assume, for the sake of this argument that British Gas had not been privatised or liberalised. Hence if there had been little or no gas generation then at least 80 per cent of British gas could have been supplied from the North Sea at fairly normal (ie pre-2021) gas prices. Some extra gas would have had to be bought at premium world LNG prices, but the social, economic and political effects on Britain would have been much much smaller than they were in reality. Even in the (I think unlikely) case that CCGTs would have been deployed to the same extent, the impact of the 2022 gas price hike would still have been considerably reduced compared to actuality.

Figure 4

Source: Energy Institute Statistical Review of World Energy

We can see the changes in UK (wholesale) gas prices in Figure 4. The massive rise in 2022 was militated by a hefty public subsidy for the domestic gas market - reducing the price for the consumer by around 30 per cent compared to the stupendously high wholesale cost (see HERE). However even by 2024 gas prices were still around 35 per cent higher than the average prices in the 2015-2019 period.

British Gas and resource conservation

There are arguments that if the gas and electricity industry had remained nationalised, then the extent of the increase in production from the North Sea would have been much less. The CCGTS tended to be funded on ‘take-or-pay’ contracts. Prospective power plant developers had to promise to pay for gas supplies in advance of project commissioning. This means there was a big incentive for the oil and gas companies to drill more and more to feed a burgeoning CGGT electricity generation market. The gas reserves would, without the pressure to feed the CCGT ‘dash for gas’, have lasted rather longer. Hence UK North Sea gas production would likely have still been higher by 2022. We can reach a speculative conclusion therefore that without privatisation and liberalisation of gas and electricity the UK may have suffered little or no energy price increases from 2021 onwards.

I interviewed Chris Hodrien1, a former Senior Researcher for British Gas, who served in the 1980s, and he commented: ‘If you are going to conserve a relatively scarce natural resource like natural gas you have to have very long term strategic national planning, as was the case up to 1986 under the former nationalised British Gas jointly with pre-Thatcher governments of the day and EU policy of the time. From 1987, the UK’s privatised-liberalised arrangements did not allow for strategic planning beyond 3-5 years and the deliberately fragmented nature of the privatised industry and the activities of the Ofgem regulator militated directly against it, despite the industry’s best attempts to proactively create a coordinating discussion forum, the ENA (Energy Networks Association).

In the 1970s, the discovery of gas in the North Sea was fairly slow (in fact, new fields are still being discovered now). It was feared (in the gas industry) in the mid 1970s that North Sea reserves would not last into the 1990s. The rate of discovery then increased so that by 1990 projected UK gas self-sufficiency was to circa 2032. In 1991, deregulation allowed the privatised ‘Dash For Gas’ to build gas fired combined cycle power stations for short term profit at a hectic rate, each with the gas consumption of a medium sized city, while simultaneously, from 1994 major gas exports to the EU were permitted for private profit by the government though the newly-built gas interconnector pipe. As a result, UK gas self-sufficiency collapsed from 2032 to 2003 and we are now (2025) importing c.55%, primarily by pipeline from Norway (‘North Sea gas, but not British North Sea gas’). It is worth noting that in the power sector, the transition from coal to gas firing made a major contribution to the UK meeting its 2021 Kyoto Agreement CO2 commitments, largely before the major takeoff of UK RE resources.’

Carbon reduction

Certainly there is a strong argument that without privatisation and liberalisation carbon emissions from the electricity sector would have been a lot higher. However, there are counter-arguments to this. A key issue here is that the arrival of gas on the electricity market considerably dampened the political drive for renewables and energy efficiency. I can recall as an energy campaigner during the 1990s and beyond being constantly annoyed by the gas industry in their insistence that gas was the way to reduce carbon emissions and reduce prices rather than renewables or energy efficiency. Not only were renewable energy programmes delayed, but proposals for energy efficiency schemes were rejected by the then Gas Regulator. Certainly the decision to privatise the industry had very little to do with climate politics, and the effects were to delay the strength and existence of energy efficiency and renewable energy programmes.

At the time, in the 1990s, the programme of privatisation, liberalisation and accelerating deployment of CCGTs appeared to be very successful in reducing energy prices. However, in retrospect, it became clear that at least a lot of the apparent consumer savings were simply a product of declining world energy prices. In those days most energy prices (including gas) were linked to oil. Oil prices had a long period of decline from 1985 to 2003 and gas prices went down with them. This gave the illusion that privatisation and liberalisation was a success.

The gas industry insisted that they should be given priority to energy efficiency and renewables on grounds of cost. Indeed in an (earlier) book I wrote, published in 1995, I said: ‘The overuse of natural gas will not only have environmental disadvantages. There could also be price rises and security problems….There could be ‘gas resource crises’ that in some ways could be even worse than the oil crises of the 1970s and the 1980s’ (see HERE pages 66- 68). The failure in the UK to put more resources into expanding renewable energy in the 1990s was a key factor in allowing the British renewables industry to fall behind the Danes, Germans and Spanish. These nations developed big wind industries which produced (and continue to maintain) many jobs making wind turbines.

Granted, a monopoly CEGB would be an unlikely candidate to develop an effective renewables industry. It was too wedded to traditional power stations, and would have lacked the competitive spur to implement a large-scale renewable energy programme cheaply. But it is more likely that renewable energy contracts would have been offered, by the Government, in a competitive fashion to independents alongside the existing CEGB.

Competition to generate renewable electricity is what happened in other countries where monopoly utilities ruled the roost (that is before they were liberalised in the early 2000s). In Denmark and Germany in the 1990s nascent wind and then solar PV industries started alongside monopoly electricity utilities. Independent companies were offered good ‘feed-in tariff’ contracts that guaranteed fixed payments for electricity generation. Much the same would no doubt have been the pattern in the UK if liberalisation of electricity generation had not occurred.

Aside from what would have been a growing renewables sector the CEGB would have carried on with its system of choosing generators on the basis of their costs (called a ‘merit order’). Prices charged to consumers were based on the ‘average’ costs of all generation used. This is as opposed to the current wholesale power market system whereby the most expensive generation in any half hour sets the price for all units of electricity. It should be also said that if there were many fewer CCGTs under a continued publicly owned system then most of the gas used would be used for non-electricity purposes.

Regrettably, the possibilities for reversing the damage done by privatisation and liberalisation are limited. Some fire-fighting has been done in the domestic supply sector through the energy price cap since 2019. But re-nationalisation s difficult because of the very large quantities of money that would have to be paid to the owners of the private electricity and gas companies to buy the shares back. Of course, in cases where the shares cost little to buy, that is a different matter! I made the case for re-nationalising retail energy supply in another blog. See HERE

Lack of Storage

A further factor that increased gas costs for the British consumer (as a result of gas liberalisation) is the lack of long term planning of gas storage. It is likely that if there had been no privatisation and liberalisation the UK would have had much more operating gas storage. This failure has cost British energy consumers a lot of money.

As Chris Hodrien told me: ‘The relative lack of seasonal winter gas storage in the UK vs. EU norms …… has meant that UK gas prices have regularly spiked in short winter cold snaps, thus putting up both gas and, indirectly, electricity prices because of the currently vital RE balancing role of the gas fired stations, in the absence of ‘true’ Grid-scale mass battery reserve. We're supposed to be buying gas from a free market in Europe, but there's clear evidence of the blocking by EU gas suppliers (with adequate gas storage) of ‘price-logical’ EU to UK gas transfer flows at these peak UK demand times which leads me to think that continental countries with large gas stores are putting their interests first. The UK government was unable to stop this activity even while an EU member, and of course Brexit has now substantially aggravated the problem, especially since jobs for contract lawyers to negotiate futures contracts have replaced jobs for engineers in the UK gas companies. Privatisation of the gas industry was done by Govt deliberately through selling off in many parts, to meet Conservative narrow-minded economic dogma to create internal within-UK competition instead of looking strategically at the global picture.’

Conclusion

The gas price crisis from 2021 is something that happened because of the dominant ‘neoliberal’ ideologies of the 1980s and 1990s and beyond. Now, I am certainly not wedded to monopoly and public ownership as an ideological counter-solution. I am a firm believer in encouraging competition where it is practical - in particular in the electricity generation sector. However we have to ask, ‘competition in what?’. If there is no real competition, and if the ‘competition’ helps deplete natural and environmental resources, then it is a bad idea.

The ‘neo-liberal’ free market choice that was put into practice at the end of the 1980s has delivered competition to use up a limited resource for the benefit of the mostly privately owned oil and gas corporations. Alas, in the 1990s, and also sadly today solutions which rely on allegedly free markets are always given the benefit of the doubt. Their advocates claim that the magical hand of a so-called free market will automatically produce the best outcome. It does not.

We should certainly keep our eyes on the objective of sustainability - in all senses of the word. What specific technologies will ensure clean energy transition in a way that protects consumers? Then, what specific incentives and regulations will promote their rapid disposition?

The alternative policy that has been followed is to encourage the maximum profit to be obtained by the oil and gas companies by selling off limited resources as quickly possible, maximising gas production, and thus increasing carbon emissions from gas. That is compared to a strategy involving energy efficiency and renewables. The latter is a democratic one since it looks to the interests of ordinary citizens and the environment rather than those of the private oil and gas companies.

You can read a lot more on this subject in Chapter 2 of my book ‘Energy Revolutions - profiteering versus democracy’ which was published by Pluto Press in 2024. See HERE

Interview June 9th 2025

Liberalization works well when you have a surplus of gas - as you have in the US. It is not surprise that it was promoted in the UK when gas production was growing and even allowed for exports - with plentiful supply, marginal prices of electricity could be kept very low.

By the way, it is not an accident that Ukraine (and its gas pipelines) entered the consciousness of the WEst in 2006 - that's the year the nthe UK became a net importer of gas again and Whitehall panicked - where will we find our energy? They tried to "steal" French and German (plentiful) storage but that did not fly, but suddenly the fact that Ukraine had been taking gas from the Russian export pipelines (something they had done every single year since 1992, without anybody caring) became a major geopolitical issue and allowed to blame an outside force for the shortsightedness of UK policy.

Interesting analysis and we must not forget that Thatcher used Nth Sea revenues to pay for 3 million on the dole ???